Far from crippling China’ technological ambitions, the US sanctions have accelerated Beijing’s transition toward a resilient, state-directed model of AI sovereignty. Through a “Triple Helix” framework that fuses immense state capital, corporate entrepreneurship, and growing R&D power of elite universities, China is systematically replacing foreign dependencies with domestic alternatives. The rapid displacement of US incumbents like Nvidia in favor of domestic architectures, coupled with surging revenues for local chipmakers, proves that China is successfully constructing an autonomous “inner cycle” of development, turning geopolitical isolation into the very catalyst for its long-term self sufficiency.

“Artificial intelligence is arguably the last technological revolution for mankind,” says Renzhen Fei, the founder of the Chinese tech tycoon Huawei, during his interview with the state-owned Renmin Ribao in early June this year. The timing of this interview is subtle yet significant. It arrives in the sixth consecutive year of US sanctions, precisely as China accelerates its pursuit of AI self-dependence amid intensifying American efforts to strategically decouple from China in critical technological sectors. Within this evolving configuration, Huawei epitomizes the institutional synthesis envisioned by the Chinese variant of the Triple Helix, serving as both the beneficiary and the vehicle of the state’s techno-industrial ambitions.

Since the inception of the Reform and Opening period in the late 1970s, China has undergone extraordinary economic transformation, rising to become the world’s second-largest economy and, notably, a dominant global manufacturing hub. While trade once climbed to its peak in 2006 – when it accounted for 64.48% of GDP – the ratio gradually declined to below 40% by 2024. This downward shift, coupled with escalating geopolitical frictions, has pushed Chinese leadership to align state developmentalism with the goals of industrial upgrading and technological independence. As China strategically pivots away from export-led growth toward high-quality, innovation-driven development, the state increasingly moves to the fore, shaping a new trajectory grounded in the Triple Helix logic of state–industry–academia interaction.

Within this top-down framework of statecraft, the central government assumes a directive role, setting strategic priorities and managing the allocation of resources across both industry and academia. Local governments, meanwhile, possess substantial autonomy and are tasked with incubating tech innovation at the regional level. The interwoven dynamics of national strategy, local experimentation, and shifting global conditions have together created a political-economic environment that positions firms like Huawei at the core of China’s technological aspirations.

Huawei’s rise illustrates this trajectory vividly. From replacing Ericsson in local arenas, to becoming a multinational corporation operating in over 170 countries, Huawei exemplifies China’s shift from technological follower to global leader in IT and AI development. Notwithstanding substantial adversities amid US suppression, Huawei not only survived the “dark ages” but diversified its business portfolio into bottleneck areas including semiconductors and operating systems. In effect, successive US crackdowns deepened Huawei’s ties with the Chinese government, intertwining the firm’s commercial interests with the state’s broader agenda of techno-industrial autonomy.

This deeper alignment is reflected in national policy. In 2022, China’s State Council published the 14th Five-Year Plan, outlining the central leadership’s vision for economic development. Positioning economic digitalization as a primary goal, the plan highlights persistent shortfalls in the domestic semiconductor industry, shortfalls fundamental to advancing the broader AI+ ecosystem. By identifying gaps in chip production, research capacity, and supply-chain integration, the plan underscores the urgency of achieving semiconductor self-reliance as a cornerstone of China’s national and strategic agenda.

In direct response, the government launched the third phase of the China Integrated Circuit Industry Investment Fund (the “Big Fund”) in May 2024, under the joint supervision of the Ministry of Finance and the China Development Bank. With registered capital exceeding ¥340 billion (approximately US$47 billion), the fund aims to channel large-scale investment into semiconductor manufacturing, equipment, and materials while strengthening upstream and downstream integration across the domestic chip ecosystem. This central-level push set the foundation for a broader multi-level financing architecture.

Provincial and municipal governments subsequently built complementary investment mechanisms to implement and extend the Big Fund’s objectives. Across industrial centers such as Shanghai, Beijing, and Guangdong, local authorities launched semiconductor equity funds and subsidy programs to support firms across the value chain. Shanghai designated semiconductor production as a top strategic industry under its 2023–2028 modernization plan, offering subsidies of up to ¥100 million and interest rebates on corporate loans. Similarly, Guangdong established a ¥28.5 billion semiconductor industry fund to attract R&D institutions and foreign-invested chip design firms, while Beijing introduced targeted subsidies to encourage enterprises to adopt domestic AI chips with an eye toward achieving near-complete self-reliance in smart-computing infrastructure by 2027. Together, these multilevel funding efforts created an increasingly synchronized ecosystem of state-backed capital, local initiative, and market incentives.

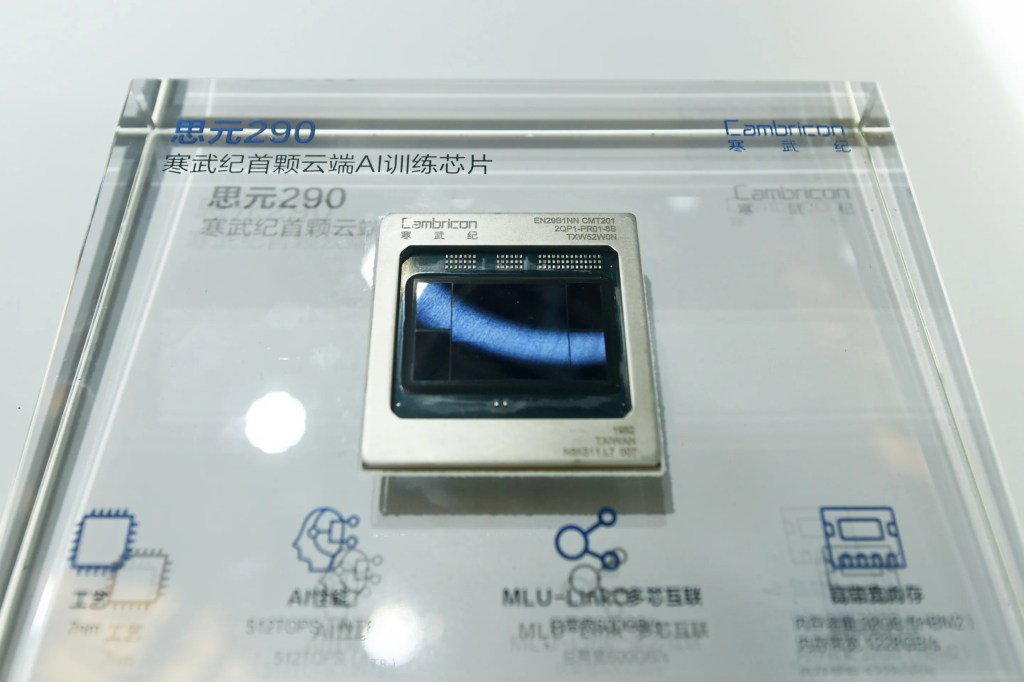

By mid-2025, the results of this coordinated financing began to materialize. Several domestic chipmakers reported expanded production capacity and increased market capitalization, fueling momentum in China’s AI sector. SMIC’s 2025 Q1 net profit more than doubled to US$188 million from US$72 million a year earlier. Likewise, Cambricon Technologies, an AI chip maker in Beijing, saw revenue surge forty-fourfold to ¥2.9 billion (~US$400 million). Similarly, Alibaba Group’s cloud intelligence unit, which oversees its Tongyi Qianwen foundation model, recorded a 38% increase in revenue during the same period, contributing to the firm’s broader post-restructuring recovery. The company attributed this expansion to rapid adoption of generative AI services by enterprises and universities, as well as the commercialization of AI-based enterprise solutions through Alibaba Cloud’s Model Studio and Qianwen API platforms. These developments illustrate how national planning, local policy, and firm-level innovation have converged to accelerate China’s self-sufficiency in AI-enabling hardware.

This domestic progress unfolded against the backdrop of shifting US–China relations. The October head-to-head meeting between the two countries sent positive signals to global markets, as Washington agreed to lower tariffs on Chinese imports to 10 percent while Beijing suspended rare-earth export controls. Yet even amid this diplomatic thaw, the world’s first company to surpass US$5 trillion in market value, and the undisputed titan of contemporary AI, NVIDIA found itself increasingly strangled in China. Once dominant in the Chinese market, NVIDIA saw its presence shrink dramatically after the Cyberspace Administration barred Chinese tech firms from purchasing its chips. “We had 95%, now zero!” lamented Jensen Huang. This extraordinary collapse was not merely a side effect of US export controls but part of Beijing’s intentional strategy to cultivate an autonomous AI ecosystem resistant to external dependencies.

If access to NVIDIA’s advanced GPUs is constrained, what substitutes does China rely on? The answer has been long in the making. Under the New Generation Artificial Intelligence Development Plan (AIDP) and Made in China 2025, universities have emerged as critical actors in China’s push for indigenous innovation. Leading institutions—such as Tsinghua university, Zhejiang university, and SJTU—were tasked with establishing AI research centers directly linked to private enterprises like Huawei and Alibaba. These partnerships facilitated the co-development of domestically designed AI accelerators, including Huawei’s Ascend series and T-head’s PPU (Subsidiary of Alibaba), effectively displacing NVIDIA’s presence in the Chinese market.

At the same time, the government’s “fusion laboratories” initiative integrated AI curricula with semiconductor design programs, ensuring that the next generation of engineers is trained on domestic architectures rather than foreign ones. With funding from the National Key R&D Program, university-led teams receive state capital to prototype AI chips aligned with national strategic goals. A prominent example is Shanghai Jiao Tong University’s collaboration with Huawei to construct one of China’s largest university-based AI computing platforms, equipped with over 600 petaflops of computing power supported by Ascend AI chips and Kunpeng processors. Through this platform, students and researchers are not only exposed to AI development environments built on domestic architectures but also actively participate in optimizing neural network models, data processing frameworks, and system integration tailored for Ascend and Kunpeng infrastructures. In doing so, SJTU serves as a national demonstration site for cultivating an innovation pipeline grounded in homegrown technologies, where pedagogy, research, and industrial collaboration converge to reduce reliance on foreign chip architectures and strengthen China’s self-sufficiency in critical computing domains.

In hindsight, massive educational investment and the redirection of procurement orders toward local firms have generated a surge in demand for domestically produced AI chips, software frameworks, and cloud services. This, in turn, stimulates the “inner cycles” of the Chinese economy, where research, production, and consumption are increasingly internalized within national boundaries. Through such coordinated mechanisms, China’s AI sector not only fortifies its technological sovereignty but also strengthens its economic resilience against external shocks.

Photo Credits: Bloomberg News